In my previous post, I talked about the importance of delivering an exceptional customer experience in banking and how regulatory compliance can hinder this process. However, it also creates an opportunity for banks to overcome this challenge through cloud computing and automation.

In this post, we’re going to take a look at open banking and how it opens up a world of opportunities for banks to further enhance the customer experience through innovation and help them:

- Create new revenue streams

- Use resources more efficiently while boosting productivity

Table of contents:

- What Is Open Banking?

- Why Does Open Banking Matter?

- The Opportunity for Open and Embedded Banking

- Open Banking and Embedded Finance

- Robust API Stack Extends Banking Services

- Leverage the Power of Open Banking with OutSystems

Before we get too far ahead of ourselves, though, let’s start by talking about what open banking is and why it matters.

What Is Open Banking?

Simply put, open banking means financial institutions will open their systems and data for use in non-banking applications. This may give their customers access to their own data, such banking balances, statements, or may allow the bank to enhance the data and add new non-bank services.

Why Does Open Banking Matter?

American consumers place a great deal of importance on being able to connect their bank accounts to innovative applications to help them budget, invest and pay bills. These “extensions” to banking are becoming the new way in which banks are competing, because the retail customer as well as the corporate banker sees tremendous convenience and value. In one study respondents said that FinTech apps:

- Saved time and money (93% and 78%, respectively)

- Provided more control (81%)

- Helped establish better financial habits (76%)

- Reduced stress (73%)

It also revealed just how important FinTech is to Americans. Amongst those surveyed:

- 80% said it’s important to be able to connect their bank account to the FinTech they use.

- 76% said that it’s a top priority to be able to connect their bank accounts to FinTech when choosing a bank.

- 69% would consider switching banks if their primary bank couldn’t connect to their financial accounts

Furthermore, 9 in 10 Americans use financial apps and services to manage some portion of their finances.

The Opportunity for Open and Embedded Banking

The open banking market is expected to reach more than $43.1B by 2026. In another analysis done by Bain Capital and Lightyear Capital, the revenue for embedded payments and embedded lending is expected to soar beyond $400B by 2030. The market opportunity for banks is huge because there are multiple ways banks are expanding:

- Embedding into non-banking applications

- Integrating non-banking apps into the banking platform

- Enabling customer-centric behavior tracking across bank lines

- Creating device agnostic micro-services

These approaches are leading banks to partner, buy and build FinTech-like firms.

Open Banking and Embedded Finance

Embedded finance is all about presenting the customer with a financial service within the shopping experience. Usually this is at checkout and can take the form of a buy now pay later option, loan and even an insurance plan.

Examples of embedded finance include Apple Pay’s contactless payments (where one’s credit and/or debit card(s) have been “added” to an e-wallet), or paying for an Uber or Lyft ride through the app itself.

Many banks have already jumped on the opportunity to take full advantage of embedded finance. For instance, Cross River Bank and Celtic Bank are working with Affirm, the company behind Amazon’s buy now pay later option. And the market isn’t exclusive to B2C. B2B is on the rise as well.

Robust API Stack Extends Banking Services

Banking as a platform and embedded finance can only happen through the use of APIs. That’s why it’s imperative for banks to build out a robust API stack to grow and thrive.

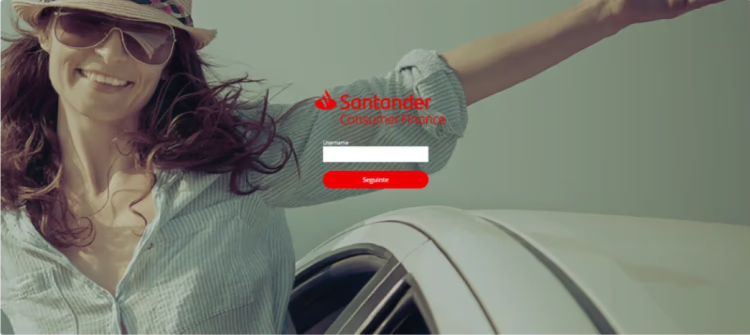

Santander Example

Santander knew the importance of leveraging the power of open banking. To do so, however, they first needed to make some significant changes on the backend.

With the help of the OutSystems platform, Santander replaced 70% of their legacy core system process—which took 20 years to develop—in only three short years.

"Working with OutSystems and KPMG, we have built a new IT architecture, replaced 70% of our core systems, and streamlined our operations. We are now executing the business vision and delivering new digital channels and solutions to lead in the consumer finance market.”

— Domingos Ferreira, IT & Operations Director, Banco Santander Consumer Portugal

With the right systems in place, Santander was able to deploy a new lending portal for auto dealers much more easily and completely change the car financing experience for customers.

As part of this roll-out,they created an end-to-end digital experience where customers could get instant credit approval and a financing offer from Santander. The customer could then shop for a vehicle that fit their payment terms. Not only did this new, digital approach simplify the process of shopping for a car, it made life much easier for dealers.

Leverage the Power of Open Banking with OutSystems

80-90% of FinTech users don’t plan to stop using financial apps anytime soon, making it clear that the appetite for financial innovation is there.

Open banking is the path forward for banks to create the products and services needed to compete and remain relevant to today’s digital world. And the OutSystems high-performance low-code platform gives your team the tools they need to quickly and easily integrate the APIs that will take your bank there.

Stay tuned for the third and final post in this series. We’ll look at how the OutSystems low-code platform can help banks respond to consumer needs and stay competitive.

To learn what OutSystems can do for your bank check out our Low-Code for Financial Services page.

Or book a demo.